The following information has been provided to assist in the

preparation of

MI Form 1040 %%MI01

Residency

Resident. You are a

Income earned by a

Part-year resident. You are a part-year resident if, during

the year, you move your permanent home into or out of

- Allocate your income from the date you moved into or out

of

- Bonus pay, severance pay, deferred income and any other

amount accrued while a

- Deferred compensation and dividend and interest income are allocated to the state of residence when received.

- Part-year residents who lived in

Nonresident. Use Schedule NR to figure your

- Salary, wages and other employee compensation for work

performed in

- Net rents and royalties from real and tangible personal

property in

- Capital gains from the sale or exchange of real property

located in

- Patent or copyright royalties if the patent or copyright

is used in

- Income (including dividend and interest income) from an S

corporation, partnership or an unincorporated business or other business

activity in

- Lottery winnings.

- Prizes won from casinos or licensed horse tracks located

in

MI Form MI1040D %%MI12

Use this form to adjust your

- Periods before October 1, 1967 (Section 271 adjustment).

If you file

- Gains or losses from the sale or exchange of

- Gains or losses from property subject to the allocation and apportionment provisions.

Enter the portion of federal gain and loss subject to

Section 271. To apportion under Section 271, multiply the gain or loss in column E by the number of months the property was held after September 30, 1967. Divide the result by the total number of months held. Enter the result in column E. For the purpose of this computation, the first month may be excluded if acquisition took place after the 15th, and the last month may be excluded if disposal took place before the 15th.

Gain from installment sales made before October 1, 1967 must

show the federal gain in column D and zero in column E. Gains from installment

sales made after October 1, 1967 are subject to

Distributions from employee’s pension, bonus or profit-sharing trust plans that are considered to be long-term capital gains (under Section 402 of the Internal Revenue Code) and capital gains distributions are not eligible for Section 271 treatment.

- Real property located in

- Tangible personal property located in Michigan at the time of the sale or owned by a Michigan resident and not subject to tax in the state where the property is located, or

- Intangible personal property sold by a

Note: Any interest expense and other expenses incurred in

the production of income from

Out-of-State Property. Gains from the sale of property located in another state are not subject to tax and losses are not deductible.

MI Form MI4797 %%MI13

File this form if you have gains from the disposition of property acquired prior to October 1, 1967, or if you have gains or losses from property subject to allocation and apportionment provisions.

The purpose of this form is to exclude from your

MI-4013 %%MI29

General Information

Complete your MI-1040 form before completing this form. Not

all Tribes have implemented Tax Agreements with the State of

Only qualifying Resident Tribal Members (RTMs) are eligible for the annual sales tax credit. An RTM is a Tribal Member whose principal place of residence is located within their Tribe's Agreement Area as described in their Agreement.

This form must be filed with the MI-1040 form.

Line 4. Tribal Affiliation of RTM. %%MI296420

Enter the 2-digit Tribal Code using the following list:

Tribal Codes

(Only those whose tribes have implemented Tax Agreements

with the State of

01 Bay Mills Indian Community

02 Grand Traverse

Band of

03 Match-E-Be-Nash-She-Wish Band of Potawatomi Indians

04 Hannahville Indian Community

07 Little River

Band of

08 Little

09 Nottawaseppi Huron Band of Potawatomi Indians

10 Pokagon Band of Potawatomi Indians

11 Saginaw Chippewa Indian Tribe of Michigan

12 Sault Ste. Marie Tribe of Chippewa Indians

Line 7. RTM Portion of Adjusted Gross Income %%MI296432

If line 6 does not include income allocable to a non-RTM spouse or both spouses are qualifying RTMs, carry amount from line 6 to line 7. If only one filer is a qualifying RTM, enter only the RTM's share of the Adjusted Gross Income (AGI) on line 7 (see "Allocating the RTM Income" below).

Allocating the RTM Income

For most types of income, the amounts should be allocated based upon whoever earned the income or owns the account. For joint accounts, federal guidelines point to state law in determining rights of ownership. Absent evidence to the contrary, co-owners are presumed to have made equal contributions to a joint account. Records or notes used in determining and verifying the allocation of the AGI should be maintained.

Additions to Income %%MI296434 %%MI296436 %%MI296438 %%MI296440

Lines 8 through 12 should include only those amounts paid to the qualifying RTM. Where both spouses are qualifying RTMs, the combined amounts of both spouses should be used. Include income received on lines 8 through 12 to the extent it is not included in AGI on your U.S. Individual Income Tax Return, Form(s) 1040, 1040A or 1040-EZ.

Line 14. Modified Adjusted Gross Income Cap. %%MI296446

If only one spouse is a qualifying RTM, enter $80,000. If both spouses are qualifying RTMs, each spouse is limited to their share of the Modified Adjusted Gross Income to a maximum of $80,000 each .

Line 16. Enter the number of months you resided in the Agreement Area. %%MI296450

Where both taxpayers are qualifying RTMs, and both resided in the Agreement Area for different lengths of time, enter the greater number of months. For example, if you resided in the Agreement Area for 6 months, and your spouse resided in the Agreement Area for 3 months, enter 6 on line 16.

Form 4884 %%MI37

If the pension received is a Military source pension, enter "M" and "MI" in fields US048240 and US040246, respectively. If the pension received is a Public source pension, enter "P" and "MI" in fields US048240 and US040246, respectively. All those pensions not coded "M" or "P" will be considered private pensions.

If pensions are received from a deceased spouse, enter the information for that spouse on Line 6.

Schedule 1 %%MI33

Line 26: Dividend, Interest, Capital Gains deduction for senior citizens %%MI330970

Senior citizens (age 65 or older) may subtract interest, dividends and capital gains included in AGI. This subtraction is limited to a maximum of $10,767 on a single return or $21,534 on a joint return.

MI-1040CR Homestead

Who May Claim a Property Tax Credit:

You may claim a property tax credit if all of the following apply:

• Your homestead is located in

• You were a Michigan resident at least six months of 2013.

• You pay property taxes or rent on your

You can have only one homestead at a time, and you must be the occupant as well as the owner or renter. Your homestead can be a rented apartment or a mobile home on a lot in a mobile home park. A vacation home or income property is not considered your homestead.

Your homestead is in your state of domicile. Domicile

is the place where you have your permanent home. It is the place you plan to

return to whenever you go away. Even if you spend the winter in a southern

state, your domicile is still

Property tax credit claims may not be submitted on behalf of minor children.

You may not claim a property tax credit if your household resources over $50,000. The computed credit is reduced by 10 percent for every $1,000 (or part of $1,000) that household income exceeds $41,000. If filing a part-year return, you must annualize household income to determine if the income limitation applies.

Which Form to File

Most filers should use Form MI-1040CR. If you are blind and own your homestead, are in the active military, are an eligible veteran or an eligible veteran’s surviving spouse, complete an MI-1040CR and an MI-1040CR-2 and use the form that gives you a larger credit. If you are blind and rent your homestead, you cannot use the MI-1040CR-2. Claim your credit on Form MI-1040CR and check the appropriate box on line 5.

Property Taxes That Can Be Claimed for Credit:

Ad valorem property taxes that were levied on your homestead in 2013, including collection fees up to 1 percent of the taxes, can be claimed no matter when you pay them. You must deduct from your 2013 property taxes any refund of property taxes received in 2013 that was a result of a corrected tax bill from a previous year.

Property Tax Credit Line 44 %%MI061580

Multiply line 42 by percentage from Table B in the instructions.

Alternate Property Tax Credit for Renters Age 65 or Older %%MI061520

Use Table A from the instructions to compute the Senior calculation.

MI-1040CR-2 Homestead

Who May File the MI-1040CR-2:

You may file Form MI-1040CR-2 if you are:

• Blind and own your homestead

• A veteran with a service-connected disability or veteran’s surviving spouse

• A surviving spouse of a veteran deceased in service

• Active military, pensioned veteran or his/her surviving spouse whose household income is less than $7,500

• A surviving spouse of a nondisabled or nonpensioned veteran of the Korean War, World War II or World War I whose household income is less than $7,500.

If you are blind and rent your homestead, claim your credit on Form MI-1040CR as a totally and

permanently disabled person.

Household Income Limits

Household income cannot be more than $7,500 for some military personnel. See line 6 on Form MI-1040CR-2 for more information. If your income is over the limit for Form MI-1040CR-2,

you may qualify for a credit using Form MI-1040CR.

Taxpayers with household income over $50,000 are not eligible for a credit in any category. The computed credit (line 11) is reduced by 10 percent for every $1,000 (or part of $1,000) that

household income exceeds $41,000. If filing a part-year return, you must annualize your income to determine if the income limitation applies.

Property Tax Credit Limits

If you own your home, your credit is based on the 2013 property taxes levied on your home, the taxable value of your homestead and the allowance for your filing category. See Table 1 in the instructions for your allowance. If you do not know the taxable value of your homestead, contact your local treasurer. If you rent your home, your credit depends on how much rent you pay, an allowance for your filing category and the millage rate on the rented property.

The millage rate is the total millage levied by your city or township, county and school district. If you do not know the rate, contact your local treasurer.

Your credit cannot be more than $1,200.

Your Credit - Line 33: %%MI078200

Enter the amount below that applies to you (maximum $1,200).

• FIP and DHS recipients, enter amount from the worksheet.

• Taxpayers who have household income over $50,000 are not eligible for a credit in any category. The computed credit (line 11) is reduced by 10 percent for every $1,000 (or part of $1,000) that your household income exceeds $41,000. If you are filing a part-year return (for a deceased

taxpayer or a part-year resident), you must annualize the household income to determine if the credit reduction applies. If the annualized income is more than $50,000, enter annualized

income on line 32 of Form MI-1040CR-2. If the annualized household income is less than $41,000,

no reduction is necessary. Then use actual household income attributable to Michigan on line 32. A surviving spouse filing a joint claim does not have to annualize the deceased spouse’s income.

To annualize income (project what it would have been for a full year):

Step 1: Divide 365 by the number of days the claimant lived or was a Michigan resident in 2013.

Step 2: Multiply the answer from step 1 by the claimant’s household income (line 32). The result is the annualized income.

Renters (Veterans Only) Line 45: %%MI07AA03 %%MI07AE03

If you rented a

name, city, landowner’s name and address, number of months rented, rent paid per month and total rent paid. Do this for each Michigan homestead rented during 2013. If you need more space, attach an additional sheet. Do not include more than 12 months’ rent. Do not include amounts paid directly to the landowner on your behalf by a government agency, unless payment is made with money withheld from your benefit.

IMPORTANT: If you rented your Michigan homestead(s) for the entire year, complete lines 46-49. If you rented your Michigan homestead(s) for part of the year, complete lines 50-56.

MI-1040CR-7 Home Heating Credit %%MI32

Who May Claim a Credit

This credit helps low income families pay their home heating costs. To see if you may claim a credit, answer the following questions:

• Are you a full-time student who is claimed as a dependent on another person’s income tax return?

• Did you live in a licensed care facility for the entire year?

If you answered YES to either of these questions, you cannot claim a home heating credit. If you answered NO to both questions, you may claim a credit if:

• Your homestead is in

• You own or rent the home where you live

• You DO NOT live in college or university-operated housing

• Your income is within the income limits listed in Tables A and B.

Standard Credit

The standard credit computation uses standard allowances established by law. Use Table A to find the standard allowance for the number of exemptions you claimed.

Alternate Credit

The alternate credit uses heating costs to compute a home heating credit. Add the amounts you were billed for heat from November 1, 2012 through October 31, 2013. If you buy bulk fuel (oil, coal, wood or bottled gas), add your receipts to get your total heating cost. Treasury may request receipts to verify your heating costs. If your claim is for less than 12 months or your heating cost

is currently included in your

rent, you cannot claim an alternate credit. You may

claim heating costs on your

Your Credit

There are two ways to compute a home heating credit: the standard credit and the alternate credit. If you are eligible to claim either credit, figure your credit both ways and claim the larger amount.

Lines 35-38: Standard credit. %%MI321995

See Table A. Find the number of exemptions you are allowed and look across to the income ceiling amount. If your household income is less than this amount, you can claim this credit.

TABLE A

2013 Home Heating Credit Standard Allowance

Your Exemptions (from line 11i) Standard Allowance Income Ceiling

0 or 1 $443 $12,642

2 $598 $17,071

3 $753 $21,500

4 $908 $25,929

5 $1062 $30,328

6 $1,217 $34,757

+ $155 for each + $4,429 for each

exemption over 6 exemption over 6

Lines 39-43: Alternate credit. %%MI322015

If your claim is for less than 12 months or your heat cost is

included with your rent, do not use this method. If your household income is

less than the maximum income for your number of

TABLE B

Exemptions and Maximum Income for the Alternate Credit Computation

Your Exemptions (from line 11i) Maximum Income

0 or 1 $13,576

2 $18,269

3 $22,967

4 or more $24,018

Line 15: %%MI322045

If your heat is provided by DTE Energy, Consumers Energy or SEMCO Energy Gas, your home

heating credit may be sent directly to your heat provider. If the credit amount exceeds your heat account balance, check this box to receive a refund from your heat provider for the overpayment, if eligible (see below). If not eligible, your excess refund will be applied toward future bills. If, after nine months, a refund balance still remains on account with your heat provider, your heat provider will issue a refund to you.

Eligibility requirements. You must have no outstanding balance with your heat provider and you must have not received heat assistance in the past 12 months.

Michigan Cities Common Form %%MI50

The following cities have agreed to accept the Common Form(CF) for computer software prepared individual returns:

BATTLE CREEK

BIG RAPIDS

GRAYLING

LAPEER

Wages %%MI500210

Wages from the Federal W-2, will be carried to the worksheet for line 1 of the CF-1040 based on the city code entered in the "State Use" field (which is to the left of the Line 18 section of the W-2). Please enter the City Code from the following list in the "State Use" field:

BC BATTLE CREEK

BR BIG RAPIDS

FL

GR

GY GRAYLING

HA

IO

JA

LA

LP LAPEER

MU

MH

PN

PR

SA

SP

WA

Renaissance Zones %%MI500480

The following cities have Renaissance Zones. The credit is prepared on the Schedule RZ of the CF-1040.

BATTLE CREEK

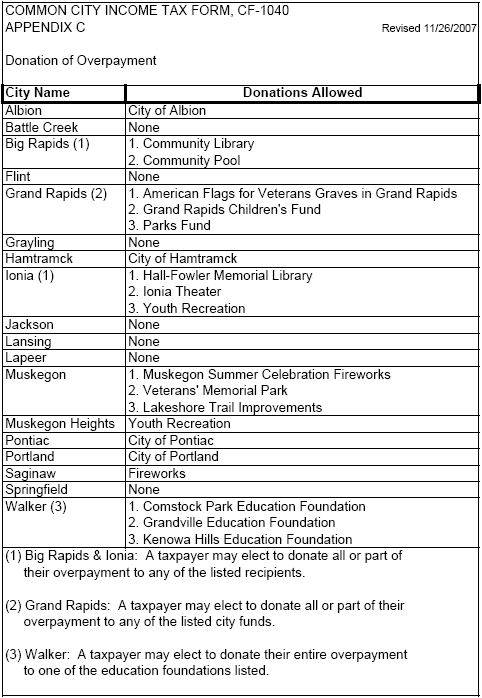

Donations %%MI509901 %%MI500560 %%MI501140 %%MI501145 %%MI501150 %%MI501155 %%MI501160 %%MI501165

The following are the available donations for each city:

Direct Deposit of Refund %%MI500895

The following cities allow the refund to be direct deposited:

Lapeer

Direct Withdrawal (ACH Electronic Payments) %%MI500905

The following cities allow the balance due to be withdrawn from the bank account entered on the return:

Lapeer

Direct withdrawal effective date %%MI500915

Enter the requested date for the electronic withdrawal if not the date that the return is processed.

Michigan Cities Renaissance Zone Deduction %%MI53

WHO MAY CLAIM A RENAISSANCE ZONE DEDUCTION

A qualified resident domiciled in a Renaissance Zone for 183 consecutive days, and qualified resident and nonresident individuals with income from rental real estate, business, profession or other activity located and doing business in a Renaissance Zone.

DEDUCTIBLE INCOME: Income earned or received during the period of domicile in a Renaissance Zone may be deducted except the following:

Lottery winnings from an instant game or on-line game won before becoming a qualified taxpayer; the portion of gains form the sale or exchange of property occurring before the qualification date; and income from illegal activities.

INDIVIDUAL WITH INCOME FROM RENTAL REAL ESTATE, A BUSINESS, A PROFESSION OR A PARTNERSHIP LOCATED AND DOING BUSINESS IN A RENAISSANCE ZONE INCOME QUALIFIED FOR RENAISSANCE ZONE DEDUCTION

1. That portion of business or professional income from business activity in a Renaissance Zone after adjustment for any net operating loss deduction and retirement plan deduction. The Renaissance Zone portion of business activity is determined via a two-factor apportionment formula, property and payroll within a City Renaissance Zone to that in the City.

2. Income from rental of real property located in a Renaissance Zone.

3. The partner’s share of partnership income from business activity in a Renaissance Zone

WHICH PART OF THE SCHEDULE DO YOU QUALIFY FOR? %%MI530008

Select Part One or Part Two

Part One is for residents domiciled in a Renaissance Zone. Part Two is for Other individuals with income from a rental real estate, business, profession or partnership located and doing business in a Renaissance Zone.

INDIVIDUALS WITH INCOME FROM RENTAL REAL ESTATE, BUSINESS, PROFESSION OR PARTNERSHIP %%MI530170 %%MI530175

For this section of Schedule RZ, residents are to use the resident column and nonresidents are to use the nonresident column. A part-year resident is to divide each line item and report the resident and nonresident portions accordingly. The income and deductions for Lines 17 and 19 will be brought from the CF-1040, based on the residency codes of resident and nonresident. For a part-year resident, please split the income and deductions into each column.

Detroit Resident Return %%MI55 %%MI550250 %%MI530240

All wages from the Federal W-2, will be carried to the D-1040 Detroit Resident Return.

Enter the location where the wages were earned.

Detroit Nonresident Return %%MI56 %%MI560250 %%MI560240 %%MI56AA03 %%MI56BA03

Wages from the Federal W-2, will be carried to the

D-1040(NR) based on the city code entered in the "State Use" field

(which is to the left of the Line 18 section of the W-2). Please enter

"DE" in the "State Use" field for wages to be taken to the

Enter the location where the Detroit wages were earned.

If all work was performed in Detroit, do not use Schedule N.

If some work was performed in

%%MI560580 %%MI560585

For the “Other Income(or losses) on Page 2, Schedule J,

enter “DETROIT” in the non-resident city name field on the Partnership K-1’s,

on the Schedule C’s and Schedule E, page 1’s to get the income (loss) to be

carried to the Detroit Non Resident return.

For the “Employee Business Expenses” line on Page 2, Schedule M, enter “

Detroit

Wages from the Federal W-2, will be carried to the D-1040(L)

based on the city code entered in the "State Use" field (which is to

the left of the Line 18 section of the W-2). Please enter "DE" in the

"State Use" field for wages to be taken to the

Enter the location where the Detroit wages were earned.

%%MI570495 %%MI570515 %%MI570525

For the “Other Income(or losses) on Page 2, Part 1, enter “DETROIT” in the non-resident city name field on the Partnership K-1’s, on the Schedule C’s and Schedule E, page 1’s to get the income (loss) to be carried to the Non Resident Column. Otherwise, the income (loss) will be included in the Resident column.